See your financial freedom date

Project your net worth year after year, test your assumptions and find out when your investments will cover your expenses forever.

Free, no credit card. Results in 2 minutes.

Age 30, testing a 15% then a 30% savings rate

At 15% saved

FIRE at 58

At 30% saved

FIRE at 49

9 years, visualized in one click

Hypothetical scenario for illustration. Your real outcome depends on your situation.

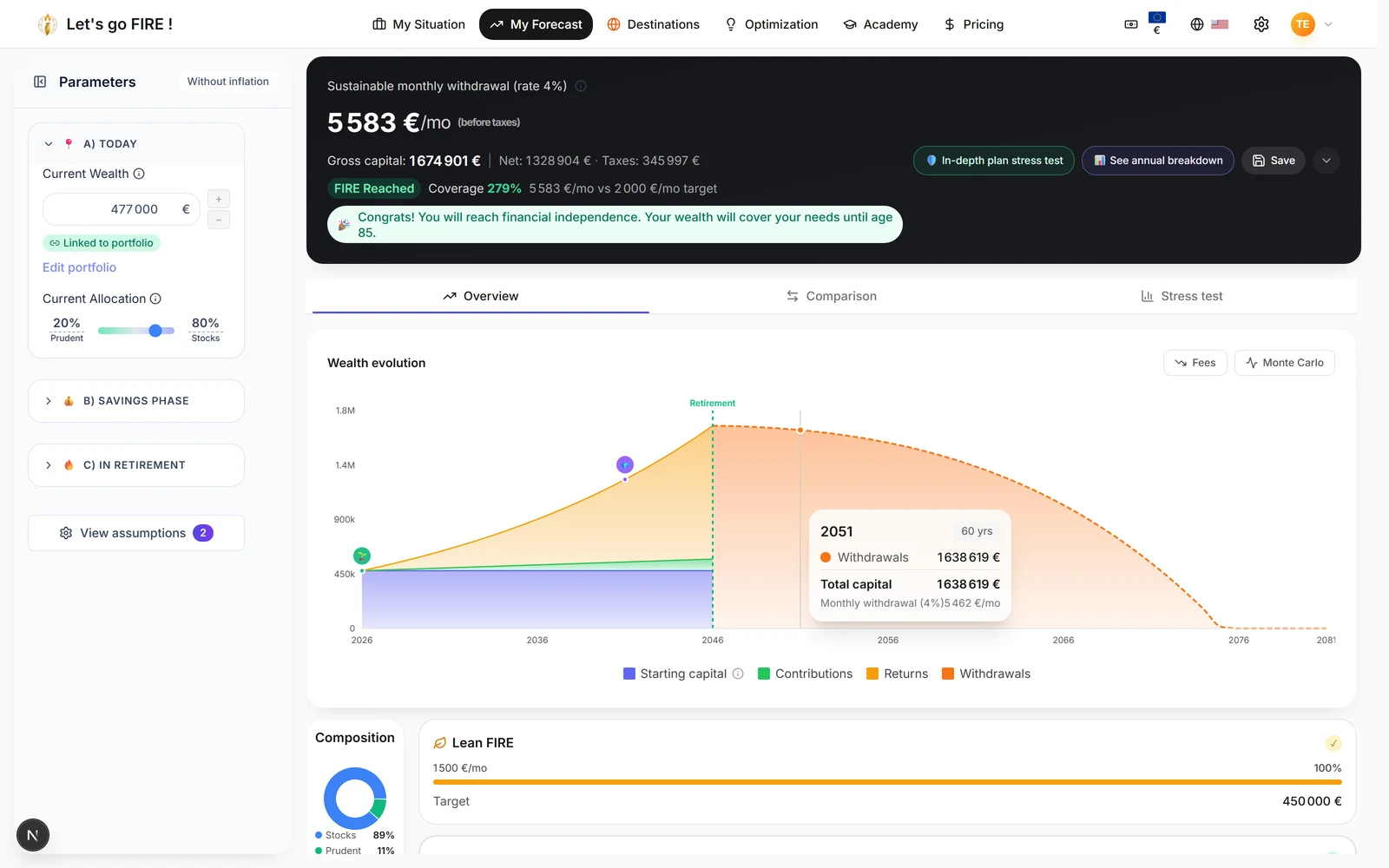

The heart of the engine: your freedom in numbers, recalculated with every setting.

Real time FIRE date

Your independence age and year recalculate with every parameter adjustment.

Three FIRE tiers tracked

Lean, Standard and Fat FIRE shown together, with a progress bar and the monthly gap remaining.

Real or nominal view

Switch between inflation adjusted constant euros and current euros in a single click.

Minimum effort solver

The tool finds the lowest contribution, or the highest spending, that still gets you to FIRE.

Every parameter is in your hands, nothing is locked.

Capital, contributions, expenses

Starting capital, monthly or yearly contributions and target expenses, all adjustable.

Returns and volatility

Set the gross returns for stocks and bonds along with their volatility.

Inflation, fees, withdrawal rate

Model inflation, the drag of annual fees and your sustainable withdrawal rate.

Monthly or yearly frequency

Display your contributions at the pace that works for you.

Well beyond the simple 4 percent rule.

Indexed 4 percent rule

The classic sustainable withdrawal, indexed to inflation or as a fixed amount.

Variable percentage withdrawal

Adapt your withdrawals to your horizon and remaining capital, year after year.

Guyton-Klinger guardrails

A spending floor and ceiling that adjust to the health of the markets.

Percentage of capital withdrawal

Income that tracks the real value of your portfolio.

Does your plan hold up against real markets? Measure it.

Monte Carlo simulation

From 100 to 10,000 market paths to measure how robust your plan is.

Capital survival probability

The success rate of your retirement, calculated across thousands of scenarios.

Sequence of returns risk

See the impact of an early retirement crash and the potential age of ruin.

A clear view of your net worth, debt included.

Multi debt tracking

Repayment schedules, payoff milestones and freed up cashflow automatically reinvested.

Real net worth

Your capital net of debt, tracked throughout the projection.

Passive income in retirement

The monthly income your portfolio will generate once FIRE is reached.

A second opinion that validates how consistent your plan is.

Consistency check

A banner flags any arithmetic inconsistency in your plan in real time.

Assumptions checker

Each assumption is rated realistic, optimistic or unrealistic against historical averages.

Inflation analysis

Measure the erosion of purchasing power and the gap between current and constant euros.

Year by year decumulation

Gross withdrawal, tax, net and viability shown for every retirement year.

PDF and Excel export

Download the full report or share it by link to review it with a clear head.

Free or Premium?

Included for free

- Real time FIRE date

- Three FIRE tiers tracked

- Real or nominal view

- Minimum effort solver

- Capital, contributions, expenses

- Returns and volatility

- Inflation, fees, withdrawal rate

- Monthly or yearly frequency

- Indexed 4 percent rule

- Percentage of capital withdrawal

- Multi debt tracking

- Real net worth

- Passive income in retirement

- Consistency check

- Assumptions checker

- Inflation analysis

With Premium

- Variable percentage withdrawal

- Guyton-Klinger guardrails

- Monte Carlo simulation

- Capital survival probability

- Sequence of returns risk

- Year by year decumulation

- PDF and Excel export

Frequently asked questions

What is FIRE and financial independence?

FIRE, which stands for Financial Independence, Retire Early, means building a pool of capital whose withdrawals cover your expenses for life. The simulator projects your net worth year after year and calculates the age at which your investments sustainably fund your lifestyle, based on your assumptions for returns, inflation, and withdrawal rate.

How do you calculate your FIRE date?

Enter your capital, your contributions, your target expenses, and your market assumptions. The simulator recalculates in real time the year and the age at which your net worth reaches your goal, and it tracks the three tiers Lean, Standard, and Fat FIRE in parallel.

What is the 4 percent rule?

It is a withdrawal rate popularized by the Trinity Study and the work of William Bengen in 1994. Withdrawing roughly 4 percent of your capital in the first year, then that amount adjusted each year for inflation, has historically funded a 30 year retirement. The simulator tests this rate and compares it with other strategies, as detailed in our methodology.

What is the difference between Lean, Standard, and Fat FIRE?

These three tiers correspond to different levels of retirement spending. Lean FIRE targets a frugal lifestyle, Standard FIRE your current standard of living, and Fat FIRE a higher level of comfort. The simulator displays them together, each with the date reached and the remaining monthly gap.

What is a Monte Carlo simulation for retirement used for?

Rather than a single average return, the Monte Carlo simulation generates thousands of random market paths to estimate the probability that your capital will last throughout your retirement. It reveals the sequence of returns risk, that is, the effect of a crash occurring just after you stop working. This analysis is part of the Premium plan.

How much do you need to reach financial independence?

As a rule of thumb, your FIRE target is 25 times your annual expenses, the mirror of the 4 percent rule: 30,000 euros of yearly spending calls for roughly 750,000 euros of capital. The simulator computes this target from your real expenses, then projects the year your wealth reaches it based on your return and inflation assumptions.

Is the FIRE simulator free?

Yes. Calculating your FIRE date, the three tiers, the full configuration of assumptions, and debt tracking are free, with no credit card. Advanced withdrawal strategies, the Monte Carlo simulation, and the PDF and Excel exports are part of the Premium plan.

Ready to know your FIRE date?

Run your first simulation in a few minutes, for free.

Free, no credit card. Results in 2 minutes.